It’s Still a Train Wreck

In February, we published a piece called, ‘The Train Wreck that is Housing’ –– it was one of our most widely read and shared articles ever.

The gist of the article is that the housing crisis we are experiencing was not caused by COVID as much as it was exacerbated by it –– and it seemed to really strike a chord with anyone in the housing business.

Spoiler alert –– 10 months later, absolutely nothing has changed.

The true cause of the current housing crisis dates back decades and is rooted in the policies and decisions by every level of governance –– from Washington, DC all the way down to your local HOA. Each rule, regulation, policy and/or mandate ultimately restricts the ability to build new housing at the rate at which it needs to be built, and at a price that is within reach of the median buyer.

COVID obviously didn’t help, it simply elevated the issue to crisis levels –– and we now are a region of over 1.3 million people and still have only +/-500 homes available to choose from.

Simply put, that isn’t nearly enough homes for sale –– and there seems to be no relief in sight.

Updating the Numbers

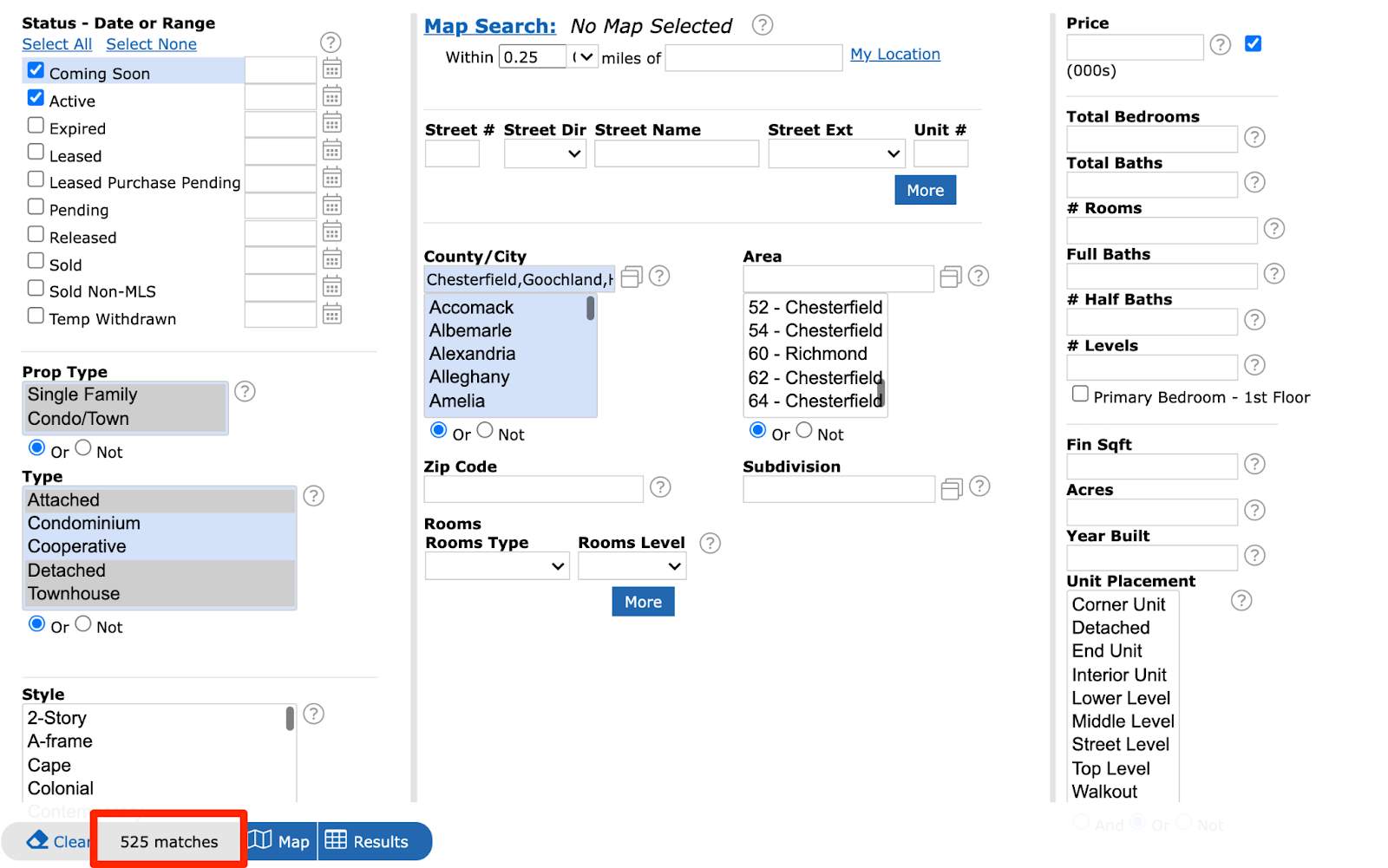

When we published the article at the beginning of February, 2021, MLS showed 527 single family homes and townhomes for sale (we did not include new homes as most were ‘to be built’ and not currently available, and we did not include condos since they are so congregated in the Downtown market.)

When we revisited the query on December 1, the number of homes for sale had barely moved –– we now have 525 homes for sale.

527 homes for sale in February.

525 homes for sale in December.

That is two fewer if you are doing the math.

And so we enter into the new year with the exact same inventory problem as we had all year –– and all of the issues that accompany it.

No New Homes

The bottom line is we have not kept pace with demand. Not by a mile.

Why? Because the layers and layers of regulations restrict the ability for supply expansion (i.e., develop more lots and build more homes) at the necessary rate to handle growing demand (i.e. –– Household Formation)

Household formation is basically when someone moves OUT of an existing home owned by someone else and starts (forms) their own household (think –– a child moves out after graduation, or 3 roommates go their separate ways.)

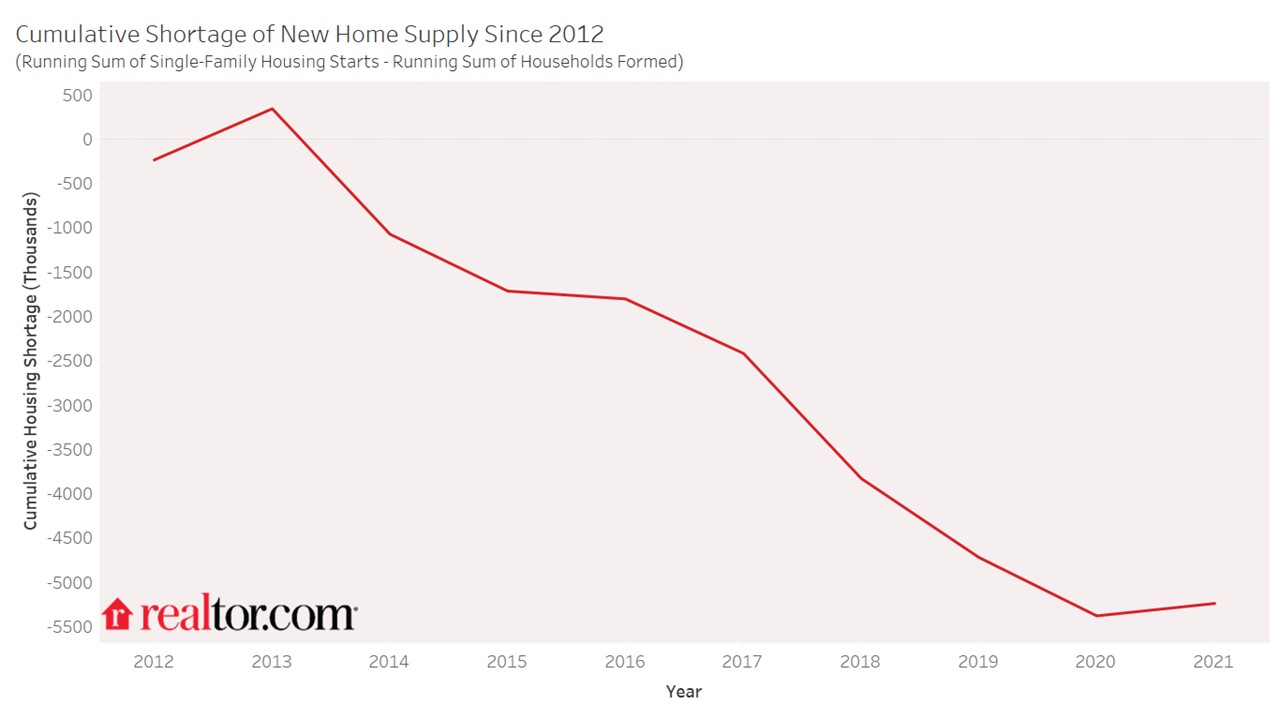

Over the last decade, the U.S. has seen over 12.4M new households form, yet only 7.5M new homes built –– leaving us with a deficit of something like 5M new homes –– and the deficit is growing, by the way.

Even if we were able to crank housing production back up to pre-crash levels, it would take something like 10 years to fully satisfy the current deficit.

This problem cannot be solved in a season or two, just so you realize. We are going to be in this pattern for some time.

The First Time Buyer is Screwed

Since there aren’t enough new homes (and the ones that get built are being built at extremely high prices), we are all left chasing the existing inventory — which means multiple buyers for nearly every home as well as logjams at the point of entry.

Do you know who pays the price for this utterly ridiculous low supply? First time buyers and other buyers with low cash reserves, that’s who.

Check out the chart below to see the dwindling number of homes available for less than $350K.

Sellers know not to accept contracts with low down payments when competitive cash offers (or substantially cash offers) are also made –– even if the debt offers may be the same price or even slightly higher. The main reason is because cash buyers are (typically) not subject to appraisals and can waive other contingencies that debt buyers cannot due to their loan type. Why take the risk of an appraiser or inspector torpedoing the deal? Cash talks …

The bottom line is that the loans typically used to enter the market were designed decades ago when market conditions looked nothing like they do today.

Pricing

Besides the fact that low down payment loans are far less effective when inventory is at crisis levels, do you know what else happens when demand outpaces supply by as much as it does? Prices skyrocket and move even further from the grasp of people who wish to purchase.

Since February, the average sales price in the greater metro region increased from $330K to $370K. If you were wondering, that is a 12% increase since the spring, and nearly a 30% increase since the beginning of COVID.

So if you stayed in the apartment an extra year and even managed to save $40K, the money you saved got eaten up by appreciation.

Sorry, but the price of entering the game went up while you were trying to save enough to enter the game.

Ownership is Healthy

Most studies show that homeowners have roughly a 40 to 50X greater net worth than renters do.

That number is sure to rise as the average homeowner’s net worth increased by another $40,000 since February simply because they owned a home –– and that is before you factor in tax savings or debt reduction.

A healthy middle class and upward mobility are what makes America, well, America — and the idea that governmental policies are degrading both of these ideals bothers me greatly. I was lucky to have housing ownership within my reach as a young adult –– and my wife and I took full advantage of it. My children will not have nearly the same opportunities as we did.

This profound change occurred in less than one generation. Think about that.

And yes, it is tempting to want to blame one side of the political aisle or the other –– please don’t.

This is not a left/right issue.

The reasons that new housing is so difficult to build and build affordably date back decades, and our collective leadership has had more than ample opportunity to reverse this trend. They simply chose not to.

And thus the market as it exists today …

Supply Side, Hello?!?

So what have the ‘powers-that-be’ done in the last 10 months?

Well, they brought down the interest rates and pumped the economy with more cash than at any period in history –– and then subsequently raised the loan limits (FNMA just announced that they increased the max loan limit to $647K from $548K.)

Solving a housing shortage with more money and larger loans is akin to trying to solve hunger with bigger forks.

Housing is a supply side issue pure and simple, and the need for new housing has never been more important. Creating even more demand into the teeth of the greatest shortage in history shows a lack of understanding of market fundamentals that boggles the mind.

Summary

To reiterate, we have plenty of buyers –– we don’t have enough houses. I don’t know why the people in power cannot seem to understand this.

Raising loan limits won’t help –– it just means more buyers.

A first time homebuyer tax credit won’t help — it also means more buyers.

Disclosing buyer side commissions won’t help –– it’s just a distraction from the real problem.

If you want to fix the problem, relax the mandates on new construction and stop making development a 2+ year endeavor. As severe as the problem is, not being able to make a meaningful dent in the deficit for 2 years because of the roadblocks in the pathway of development just means more of the same for the foreseeable future.

Sorry, millennials, I hope you like your landlord and their record-breaking rent increases.

Similarly, make it easier to not just build houses, but to build them more affordably. The National Association of Home Builders pegged the cost of compliance in the price of a new home approaching $100K.

To reiterate yet again –– ONE HUNDRED THOUSAND DOLLARS IN A NEW HOME’S PRICE IS RELATED TO COMPLIANCE –– and it is passed directly to the consumer.

There is an entire generation that is being denied the opportunity to own the most important asset to build wealth.

So I will modify the mantra from February –– ‘1.3M people / 500 more expensive homes for sale’ –– and no one seems to be working on the problem.