The Train Wreck That is Housing

In case you hadn’t heard, we have an inventory problem.

Right now, in a region of 1.3M people, we have +/- 500 homes for sale.

I know what you are thinking –– ‘Yeah, yeah, yeah, we know, low inventory. We get it. Not a lot of houses. Thanks. Can you maybe talk about something else for once?!?’

Sure. We can talk about how we got here.

The Slowest Wreck Ever

Each time I think about how we got here, I am reminded of the scene in Austin Powers where he runs over the bad guy with a steamroller. The joke is obviously how slow a steamroller moves and how easy it would have been for the guy to get out of the way.

The speed at which we have arrived at this point has taken years (if not decades) and we have had more than ample opportunity to steer clear of the situation –– we just haven’t done it.

So, here we are with 500 houses available in a region of 1.3M people.

How Did We End Up Here?

I think the simplest answer is that no one is in charge.

In the same way that the financial crash of 2008 was allowed to happen because about 10 different regulatory agencies all managed to NOT pay attention all at once, housing is in the same boat.

Super Bowl winning coach Bill Parcells famously said that when you have two quarterbacks, you have none (implying two leaders means no one is actually leading). So when you have something like 20 different agencies and / or entities that have input into the housing market, you end up with the ridiculous situation we are in.

And thus 1.3M people / 500 houses for sale.

Who Holds Sway?

The short answer is everyone, yet no one at all.

Below is a list of every entity that I can think of which has legitimate input into the housing market. And by input, I mean they have the power to make housing more difficult or expensive to create.

At the federal level, we have the following alphabet soup of agencies who all impact housing:

- The Federal Reserve (The Fed)

- Federal Housing Administration (FHA)

- Housing and Urban Development (HUD)

- Consumer Federal Protection Bureau (CFPB)

- International Trade Administration (ITA)

- Department of Energy (DOE)

- The General Services Agency (GSA)

- Internal Revenue Service (IRS)

- Army Corps of Engineers

- Environmental Protection Agency (EPA)

At the state level, these guys pile on the regulations put forth by our friends in Washington, DC:

- Department of Environmental Quality (DEQ)

- Department of Housing and Community Development

- Virginia Historical Society

- General Assembly

- Virginia Housing Development Authority (VHDA)

At the local level, it’s more about the enforcement of zoning codes and approval of development:

- Richmond Redevelopment and Housing Authority (RRHA)

- Board(s) of Supervisors

- Office(s) of Planning and Zoning / Zoning Appeals

- Office(s) Building Permits

- Historical Societies and Historic Protection Overlay Districts

At the community level, don’t forget about:

- Homeowners associations

- Condominium associations

- Architectural review boards

- Concerned citizens

And finally, there are several overarching pieces of legislation that govern our industry:

- Fair Housing Act

- Dodd-Frank Wall Street Reform and Consumer Protection Act

- Chesapeake Bay Protection Act

Each one of these agencies / groups / acts, in some way, shape, or form, limits the places where homes can be built, limits the type of house that can be built, increases the cost of building a home, and increases the cost of compliance with any form of real estate transaction.

1.3M people / 500 houses for sale.

The Public is Also Complicit

So after we look at the sheer number of organizations and government departments that have their say, the public then gets to voice their opinion, too. Trust me, they are not fans of any form of development.

The residents of the towns, counties, and communities who sit in traffic, attend the schools, pay the taxes, and otherwise live in the places where development occurs, don’t want any more of it –– especially if development means more affordable forms of housing.

The dreaded NIMBYs (Not In My Back Yard) in any community will almost always vehemently fight any development and / or vote out the supervisors who allow it.

NIMBYs don’t set policy in the way that our elected officials do, but they have a very real impact on housing –– albeit in a far less official, but extremely powerful, way.

1.3M people / 500 houses for sale.

Affordability is Gone

As this post is written, the lack of supply, when it intersects with the mortgage rate demand-driven frothiness, has created a toxic stew for the very segment whose needs are the most fragile –– the segment with limited savings and average incomes.

Housing affordability is now officially a thing of the past as each and every home that can be afforded by the median income earners in a region is bid up beyond their ability to secure it.

If you don’t own, you rent –– and I don’t need to tell you who benefits from tenancy. It sure isn’t the tenant.

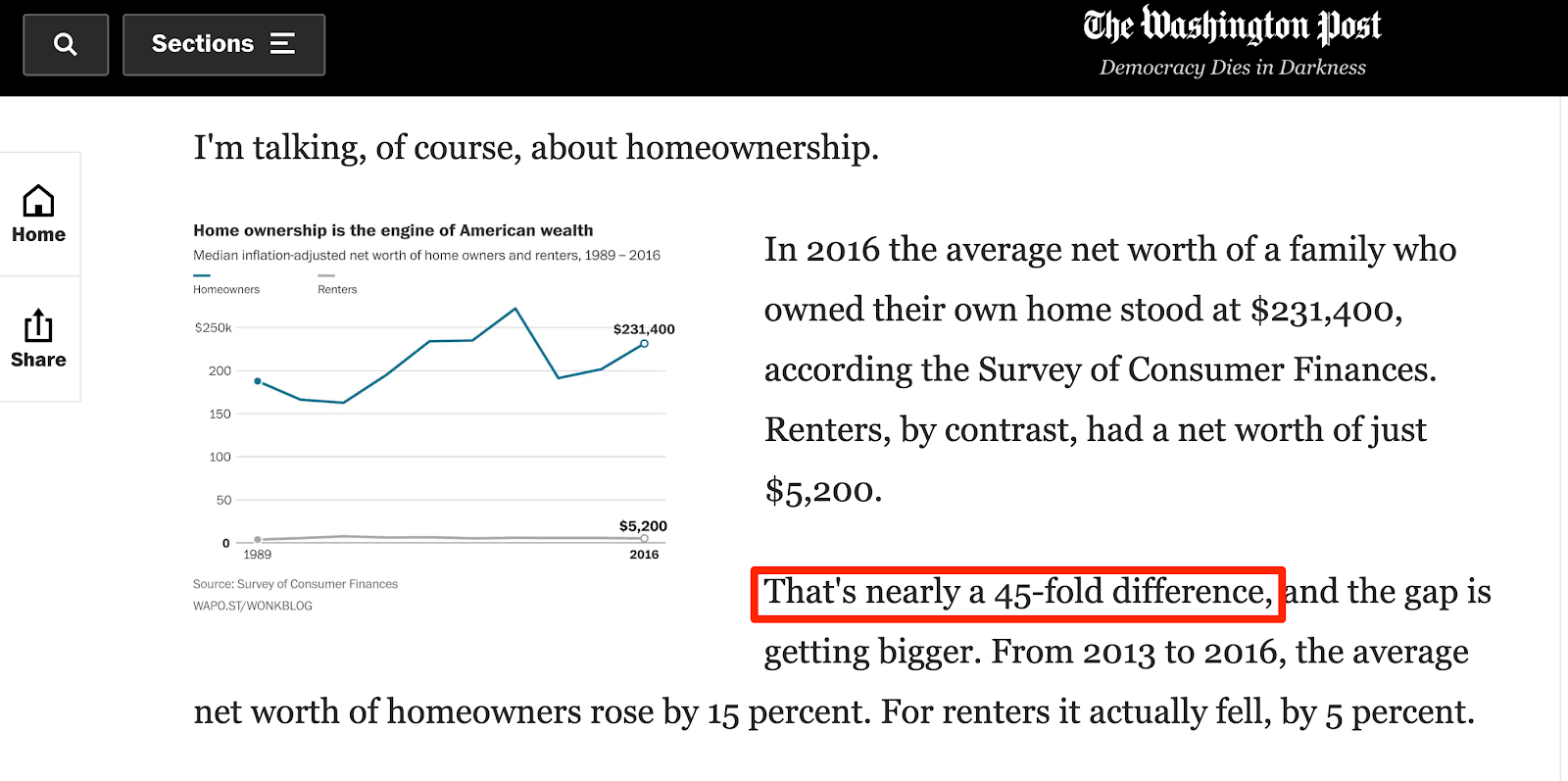

Recent studies show that the average net worth of a homeowner is more than 40X the tenant –– and getting worse.

And I think that sucks.

1.3M people / 500 houses for sale.

Housing Costs

Right now, we simply can’t build housing fast enough, or affordably enough, to change the trajectory we are on.

Why?

- ‘You can’t build there –– or there –– or there,’ says the Corp of Engineers.

- ‘The framing needs to be more robust,’ says the code enforcement folks.

- ‘Don’t forget we are now in an earthquake zone,’ says the Building Department.

- ‘We now have a net-zero energy mandate,’ says the DOE.

- ‘That isn’t a capital gain,’ says the IRS.

- ‘We need a tariff on lumber imports,’ says the ITA.

- ‘You have to sell 50% of the condos before we will loan in that complex,’ says Freddie Mac.

- ‘Sorry, we know you work two jobs, but we can’t count that hourly income,’ says FHA.

- ‘You realize that is now a flood plain,’ says FEMA.

- ‘And wetlands, too!’ says the DEQ.

- ‘We can’t have an inspector out there for two weeks,’ says the permit department.

- ‘You need to comply with the new disclosures.’ says the CFPB.

- ‘You can’t build them that close together,’ says the Planning Department.

- ‘We will need you to pay for the new school,’ says the Board of Supervisors.

- ‘We need brick on the front,’ says the Architectural Review Board.

- ‘We need better landscaping,’ says the Homeowner’s Association.

- ‘How dare you build those here! NO WAY!!’ says every NIMBY.

- ‘You are one of 17 offers,’ says the Realtor.

- ‘Sorry, it didn’t appraise,’ says the appraiser.

I could go on and on, but I think I have made my point.

1.3M people / 500 houses for sale.

Hypocrisy, Ineptitude, or Apathy?

I can assure you that no government agency has the mandate to PREVENT homeownership –– but when you look at the policies, you have to wonder.

Do they not realize the impact? Do they not care? Or are they just tossing some lip service at the issue in order to secure votes? Your answer probably has a lot to do with your political views –– but the result is the same.

You cannot talk about income inequality on one hand and then mandate net zero energy homes on the other.

You can’t complain about the lack of affordable housing while you simultaneously drive lumber costs through the roof with trade wars.

And above all else, you can’t call homeownership the ‘American Dream’ and then put as many roadblocks in front of it as you do.

1.3M people / 500 houses for sale.

The Bottom Line

The bottom line is that a new caste system is emerging (more like solidifying, really) that is based largely on homeownership. It’s easy to blame COVID, but available inventory (especially affordable inventory) has been on the decline for years and it has finally culminated in the conditions we are currently experiencing.

Purchasers who need any form of low down payment financing simply cannot buy right now. Besides the fact that bidding wars drive prices above the ability for the median buyer to qualify, sellers know that cash buyers don’t have to worry about appraisals and repairs.

If you require a low down payment loan or grant funds to buy a home, don’t bother –– your offer is not going to win.

The message has become, ‘Sorry renter, you don’t get to experience the greatest period of equity growth in the history of our country. The American Dream is not for you.’

Housing is one of the most reliable ways to build wealth –– and the policies that have been in place for decades now have finally culminated in a market where homeownership is increasingly a proxy for ‘the haves’ vs. ‘the have nots.’

1.3M people / 500 houses for sale.

Don’t Blame the Other Side

Just so you realize, the policies are not the fault of the left or right –– so don’t feed me the ‘Obama this’ or the ‘Trump that’ junk. I also don’t want to hear about COVID.

This train wreck has been decades in the making –– both sides of the aisle and all levels of government have blood on their hands.

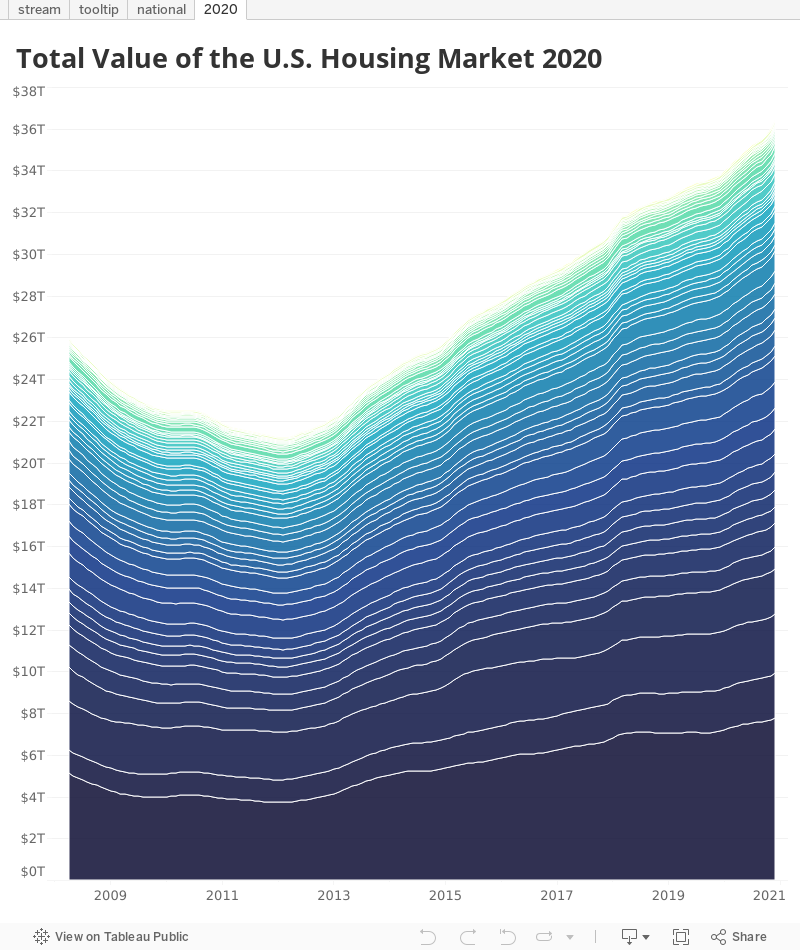

Want to see a telling graph? Look at what has happened to the number of homes for sale between $150,000 and $300,000 in the past 5 years.

I don’t know how to illustrate the issue any more clearly.

Yes, COVID has been a catalyst, but when COVID is no longer dominating the headlines, what about this trendline makes you think it will reverse itself?

1.3M people / 500 houses for sale.